Hybrid projects aren’t new. The industry has been exploring the benefits of co-locating different types of renewable generation and storage technology for many years now. But while there is lots of talk of “energy parks”, “virtual power plants” and other hybrid concepts, in reality we continue to see the vast majority of wind, solar and storage plants being built out on a standalone basis.

There are however signs that hybrids are becoming more mainstream. Less than 10% of the UK’s current battery storage fleet is co-located (around 160 MW), but the pipeline of co-located storage amounts to around 7 GW across more than 300 projects – representing around 20% of the overall storage development pipeline.

At the same time, owners of large operational wind fleets are exploring ways to augment and optimise their existing assets by adding solar, battery storage and even green hydrogen technology to their sites. It is safe to assume that by 2030, hybrid projects will form a mainstream part of our energy landscape.

But not all hybrid projects are created equal. Ranging from basic site sharing arrangements to fully integrated hybrid plants, there are many options in between each with its pros and cons. For example, a project where solar and storage are physically co-located but don’t share a grid connection means there are no complicated interfaces, but there are limited cost savings and no optimisation between the individual components’ revenue streams. Compared to a fully hybrid site that operates as a single commercial entity, where there’s a shared substation and HV equipment – this can lead to substantial grid cost savings, but joint optimisation and offtake agreements are not yet well-established and may be perceived as high risk by investors.

It’s vital to look at the business case for hybridisation as energy prices reach unprecedented highs. As a result, “behind the meter” options are growing in popularity. This approach to on-site generation can form a key advantage for residential, commercial and industrial settings to save on energy costs. Solar PV is the most popular form of behind the meter generation due to its low cost, simple installation and straightforward permitting. Since the UK has phased out its lucrative feed-in tariff for small-scale renewable installations, the focus is on maximising self-consumption – which boosts the business case for hybrid solar and storage.

The solar generation profile with its mid-day peak typically does not fully line up with demand, whether from an individual residential property or a large industrial site. Any excess generation would need to be curtailed or exported to the grid at a low tariff. A co-located battery storage system can help smooth out the mid-day peak and store electricity for when it is needed. Many commercial and industrial players are combining this with on-site EV charging infrastructure for their staff and/or fleet vehicles.

We are also seeing more and more energy suppliers offer time-of-use tariffs which incentivise customer flexibility, and again in this scenario, batteries can help to maximise savings. A hybrid system may also help access additional revenue streams by providing frequency response and demand side response services (if the grid connection allows). In the UK, aggregators such as Limejump and Flexitricity are successfully dispatching virtual power plants made up of small-scale solar and storage on the balancing mechanism. German solar and storage provider Sonnen is pursuing a similar model with various international partners.

Germany remains the leading residential solar/storage market in Europe, with around €1.6 billion in sales in 2021 (23% growth over 2020). Other major markets for the behind the meter segment include Italy, Austria, the UK, Australia and the USA. The growth in residential solar and storage is closely coupled with electric vehicle sales.

In front of the meter, developing, constructing and operating a large-scale hybrid plant is undoubtedly more complex than focusing on standalone technologies. Nevertheless, there are a number of key drivers for hybridisation.

Firstly, access to the grid is becoming expensive and highly competitive. This applies particularly to island nations like Ireland and the UK which already have significant renewables penetration, but also to countries like Spain and Portugal, where the existing grid infrastructure is at its limits.

If a grid connection can be secured, it may involve curtailment schemes, such as active network management in the UK, which can result in significant losses that the generator is not compensated for. Developers are therefore looking to maximise the use of their precious grid connections with multiple complementary generation and storage technologies. This is often referred to as an “energy park” concept, and can be seen favourably by planning authorities as it limits the visual impact of new energy infrastructure.

Even if no grid connection can be secured, green hydrogen is starting to offer an alternative route to market for renewable generators.

Renewable generators are increasingly exposed to merchant risk. This primarily applies to new projects that are being built on a subsidy-free basis. A common approach is to secure a PPA where, for example, 70% of the electricity output is sold under a fixed price, and the rest is sold on the wholesale market.

Even CfD-style (Contracts for Difference) support regimes are starting to exclude periods where wholesale pricing is negative. Older sites that are coming out of legacy subsidy schemes such as the UK Renewables Obligation will also need to prepare to operate under a more merchant-focused world.

Furthermore, price cannibalisation is a growing concern – wind is already the dominant price maker in the UK electricity market, and sunny days regularly lead to low and negative pricing in mainland Europe. Projects will need to protect themselves from this if they have any exposure to wholesale prices. However, merchant price volatility also represents an opportunity to maximise revenues for generators, in particular via arbitrage and balancing.

Of course, each technology component of a hybrid project has to stack up individually. Hybridisation is rarely going to make or break a business case, however, our experience suggests you can boost internal rate of revenue (IRR) by 2% or more through co-location. The majority of this uplift derives from Capex savings, but we expect that revenue-related benefits will increase throughout the coming years due to the merchant dynamics described above.

As an industry, we have historically been very focused on annual energy yield predictions. But in this new merchant and hybrid landscape, it’s no longer just about how many MWhs are being fed into the grid, we need to understand and optimise when these MWhs are being injected. New approaches to time series yield and revenue analysis are essential to help investors understand the value of a project.

So how does it work?

Solar is the obvious partner for battery storage due to its predictable resource profile. In lower-irradiance climates, solar farms rarely produce at rated capacity, and of course no solar farms export any power during night-time. The relatively predictable solar generation profile lends itself to peak shifting and arbitrage, and the battery remains free to provide ancillary services outside of daylight hours.

More than half of the planning applications for large-scale solar farms we see in the UK today have provision for storage co-location, although developers may choose not to build out the BESS immediately.

Most utility-scale combined solar and storage projects are AC coupled. This means that the BESS has a separate inverter, rather than sharing the solar inverters. The two assets can be controlled more independently and constructed on a quasi-standalone basis. When adding storage to an existing renewable generator, AC coupling is by far the most practicable option. AC coupled designs are highly standardised at this point and remain the most popular choice for solar-storage hybrids. An example is the landmark 350MW Cleve Hill site, which is the first combined solar and storage project of this scale to be consented in the UK.

Figure 1: AC coupling

Figure 1: AC coupling

The alternative is DC coupling, where each section of the solar array shares an inverter with a section of the BESS. Individual BESS units are co-located throughout the solar array next to the inverters, rather than being installed at a separate BESS compound. The key advantages of DC coupling are saving cost on inverters, and being able to store clipping losses when the DC power generated by the solar modules exceeds the inverter AC rating.

DC coupling is a less common configuration as it is more challenging in terms of technical and commercial separation of the assets. A DC coupled asset is a true hybrid that participates on the market as a single entity, whereas AC coupled systems can separate the activities of the solar and storage components. The common inverter also acts as a single point of failure, which can be a drawback. At present, the US is the only major storage market where there is significant demand for DC coupled systems, which is related to the federal investment tax credit.

Figure 2: DC coupling

Figure 2: DC coupling

Clearly, it is important to make a decision on coupling arrangements early on in the development stage as this will influence the design and permitting process. Any import requirements should also be captured from the start – if a project has to retrospectively add import capacity to its grid application, there is a risk of falling to the back of the grid queue and delaying or even losing access to the grid.

It is important to note that in the UK, around 80-85% of BESS revenues still come from ancillary services, which a standalone project can provide just as effectively as a hybrid BESS. However, industry expectations are that the storage revenue stack will gradually move towards wholesale trading and balancing. For these applications, a solar-storage hybrid may have an advantage over a standalone BESS which has to charge from the grid.

In contrast to solar farms, wind farms have much higher capacity factors and frequently export at rated power for hours at a time. In a constrained grid export scenario, this limits the amount of time a co-located BESS could be active. In order to effectively peak shift wind generation, a very large BESS (more than six hours) would be required, which is unlikely to be financially viable.

Examples of wind-battery hybrids, such as Vattenfall’s Pen y Cymoed and Equinor’s Batwind projects remain rare. Many more wind farm owners and developers are exploring co-location of solar and onshore wind generation. The wind and solar resources are complimentary to a certain extent – the windiest periods tend to occur during the winter months and during night time, when the solar resource is low. This allows for over-sizing of the combined generation capacity with respect to the grid export limit, without incurring prohibitive curtailment losses.

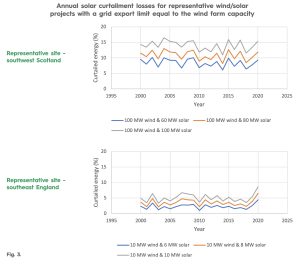

At Natural Power, we’ve analysed curtailment losses for different wind-solar sizing scenarios. A representative profile for two sites in Scotland and England are shown below. The analysis assumes:

- The grid export limit is equal to the wind farm capacity

- Solar generation is curtailed at times when the combined wind-solar output exceeds the grid export limit

- Solar curtailment losses are calculated as a percentage of the uncurtailed solar generation potential

- A 20-year period is modelled to assess the inter-annual variability of curtailment losses

It can be seen that windiness levels are a key driver of hybrid curtailment losses. The wind farm in Scotland operates at rated power much more frequently than the wind farm in England, leaving less headroom in the grid connection for the solar farm. This is somewhat counteracted by the solar resource being lower in Scotland, and therefore having fewer periods where the solar farm is exporting at or near its maximum.

The inter-annual variability of the wind and solar resource also causes some years to experience particularly high or low curtailment losses.

Even in the most aggressive curtailment scenario modelled, where the combined wind and solar capacity is double the grid export limit, losses remain fairly moderate – approximately 12-16% for the site in Scotland, and 3-9% for the site in England. The optimum sizing, taking into account grid capex savings and other costs, will be project-specific. However, these results suggest that it is worth exploring wind and solar co-location. For example, in a scenario where solar can be retrofitted onto an existing wind grid connection with no additional export capacity being available.

Figure 3: Annual solar curtailment losses for representative wind/solar projects with a grid export limit equal to the wind farm capacity

Figure 3: Annual solar curtailment losses for representative wind/solar projects with a grid export limit equal to the wind farm capacity

Not every wind farm site is suitable for solar co-location. Steep terrain, forestry and low irradiance may rule out solar development. However, in markets like the UK, there are many existing wind farms located in flat, sunny areas where new wind development or repowering would likely be impossible from a permitting perspective. These sites could be prime candidates for solar co-location.

With any form of retrofitting to an existing subsidised project, complex sub-metering arrangements may be required to retain the subsidy support. The amount of energy generated by each technology must be clearly established, and if a battery is involved, it is essential to be able to separate times where the battery is charging from the grid versus from co-located renewable generation. In the UK, the regulator (Ofgem) has published guidance to help developers and asset owners manage these complexities.

Green hydrogen is a rapidly growing sector in many European markets, with governments putting incentive schemes in place to support the development of co-located renewable generation and green hydrogen infrastructure.

Green hydrogen denotes the process of converting renewable electricity to hydrogen via an electrolyser. This is a subset of so-called “power-to-X” applications where electricity is converted to another energy carrier that may be more convenient to store or transport.

Hydrogen can be used in a variety of applications such as fertiliser, industrial processes and transport. Green hydrogen is seen as a key enabler of long-duration energy storage in a net zero grid, where renewable generation will need to support seasonally variable demand. This is particularly interesting for countries with significant offshore wind capacity, where there may be prolonged periods of low or high wind generation that need to be smoothed out.

For wind and solar projects that cannot secure a grid connection, for all or some of their capacity, co-locating with green hydrogen offers an alternative route to market. The key challenges are to identify an offtaker and means of transporting hydrogen to this offtaker. The majority of such hybrid developments to date are located close to industrial facilities that already use conventional hydrogen generated from fossil fuels. To support the scale of green hydrogen targeted by governments, investment in wider hydrogen transport networks will be required.

Notable renewable/green hydrogen projects include Iberdrola’s Puertollano project in Spain, which became operational in 2022 and combines a 100 MW solar farm with a 20 MW electrolyser to supply a local ammonia factory; ScottishPower Renewables Whitelee project in Scotland, which involves co-location of solar, BESS and green hydrogen and an existing onshore wind farm; and Orsted and ITM Power’s Gigastack project in northeast England, which will feature a 100 MW electrolyser fed by Hornsea 2 offshore wind farm.

Most hybrid projects are oversized with respect to their grid export limit. This inevitably leads to a risk of export conflict, such as when the operation of one component has to be restricted in favour of the other.

Managing these conflicts from a commercial perspective, and ensuring revenue impacts remain minimal, can be simple or complex. For example, if new solar generation is added to an operational wind farm that benefits from lucrative subsidies, the obvious strategy is to always give precedence to wind generation. For a new build solar and storage project, the dispatch strategy will depend on a number of revenue streams, both contracted and merchant. Trading and optimising service providers will seek to make choices for the day ahead and even in real time.

In practice, export conflict presents less of a risk than developers and investors may fear. Spot prices tend to be low when wind and solar are exporting at their peak, and the local network may be constrained. It therefore is unlikely that a co-located BESS would generate significant revenue from exporting power for arbitrage or balancing during these times. For the majority of solar-storage projects that we have seen at Natural Power, the impact of export conflict on revenue has been well below 10%.

As we move towards a net zero grid, the challenge of integrating renewables is undoubtedly becoming more complex. Co-location and hybridisation of different renewable generation and storage technologies is essential to building a cost-effective power system.

There are numerous benefits and this approach will minimise the need for costly grid reinforcements where possible, avoid major curtailment losses during times of high wind-solar resource, manage revenue risk for generators in an increasingly merchant environment, and help to decarbonise hard-to-electrify sectors via power-to-X applications.

The challenge for developers is to work out which combination of technologies is best suited to their site, and how to manage commercial and physical interfaces between the different components of a hybrid project. Regulation needs to evolve quickly to accommodate this growing market, and both industry and government bodies have a role to play in driving standardisation of designs and contract structures.