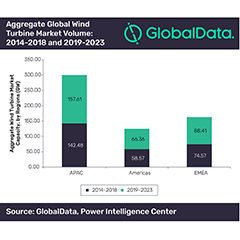

Asia-Pacific (APAC) is expected to lead the wind turbine market with an annual installation capacity of 33.14 gigawatt (GW) by 2023, largely driven by onshore deployment; followed by EMEA and Americas with capacities of 19.9GW and 11.7GW, respectively, according to GlobalData, a leading data and analytics company.

The company’s latest report ‘Wind Turbine, Update 2019 – Global Market Size, Competitive Landscape and Key Country Analysis to 2023’ reveals that the buoyancy in the market is largely due to the global investment trends in renewable energy to address power sector challenges.

Bhavana Sri Pullagura, Power Analyst for GlobalData, comments: “The need to address electricity demand, supportive government policies, feed-in tariffs (FiTs) and other financial incentives, growing wind turbine sizes, and declining operations and maintenance costs are primarily driving the market for wind turbines. Furthermore, the market opportunities are attracting a plethora of potential investors and stakeholders driving down equipment costs, promoting technology development, and thereby creating a feasible market for wind equipments such as turbines.”

In the forecast period (2019–2023), wind turbine installations are expected to reach an aggregate of 312.39GW. APAC will continue to lead the market, with an aggregate of 157.61GW of installed capacity, followed by EMEA and Americas with 88.41 GW and 66.36 GW, respectively.

The APAC region led the onshore wind turbine market by registering an aggregate capacity of 138.20GW between 2014 and 2018, and will continue to do so in the future. The need to improve access to electricity, increasing consumption trends and strong industrial market are primary driving factors for onshore wind turbines market.

The growth in the APAC region is largely contributed by China, which has established comprehensive development plans focused on using renewable energy to sustain its growth and ambitions of becoming a global leader in wind technology development.

In the offshore market, EMEA dominated the market and will continue to do so reaching 4.77GW in 2023. EMEA’s dominance is largely driven by the European market. The strong technology base in Europe, favorable wind conditions and increasing effectiveness of offshore wind turbines have contributed to the large scale deployment of offshore wind technology to capitalize on the significantly larger resource.

Bhavana concludes: “The utilization of renewables is seen as a suitable mechanism to wean away from the resilience on fossil fuels, which has contributed to a myriad of environmental and economic problems. The global commitment to curb emissions, need to circumvent geopolitical risks impacting the supply of fossil fuels, transition towards low carbon emitting economies, and increasing demand for electricity will drive the wind turbines market.”

About GlobalData

4,000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, technology, energy, financial and professional services sectors.